Do you ever feel overwhelmed about money? How can you control your money so that your money doesn’t control you?

Even if you haven’t chosen to study HSC Economics or HSC Business Studies (shame on you) I’m going to show you how/why to budget and why you need to be financially literate.

“Financial literacy is the ability to make informed judgements and to take effective decisions regarding the use and management of money.”

– 2014 ANZ Survey of Adult Financial Literacy in Australia

This means that you can stay in control of your finances and make short and long-term choices with your money that positively impact your life.

Dealing with money is stressful. A growing percentage of people (22%) now feel like they are not in control of their finances. But it doesn’t have to be stressful; below I touch on some key aspects of financial literacy and some ways you can stay in complete control.

Now let’s look at budgeting and what you can do today to feel in control.

What is budgeting?

Preparing a budget is a great first step in navigating your way through the financial maze of adulthood.

A budget is simply a way to provide funds for a particular purchase or activity. A budget helps you determine what your total income is, what your total expenditure is, and how much you have left over to save and spend on other things later.

In high school, I had limited income but also limited expenses. I earned a little bit of pocket money from my parents (throwing out the garbage was my chore of choice) as well as from some part time work. My main expenses included my phone plan, food and other entertainment.

So although you may have limited income and limited expenses now, it’s important to get into good habits!

Preparing a budget is simple!

Preparing a simple budget can help you see where your money is coming from and where it is going. To get a snapshot for yourself, for one week, simply write down everything that you earn (your income) as well as everything that you spend (your expenses).

Preparing a budget will let you see how much disposable (extra) income you have each week and give you an idea of ways that you can increase this.

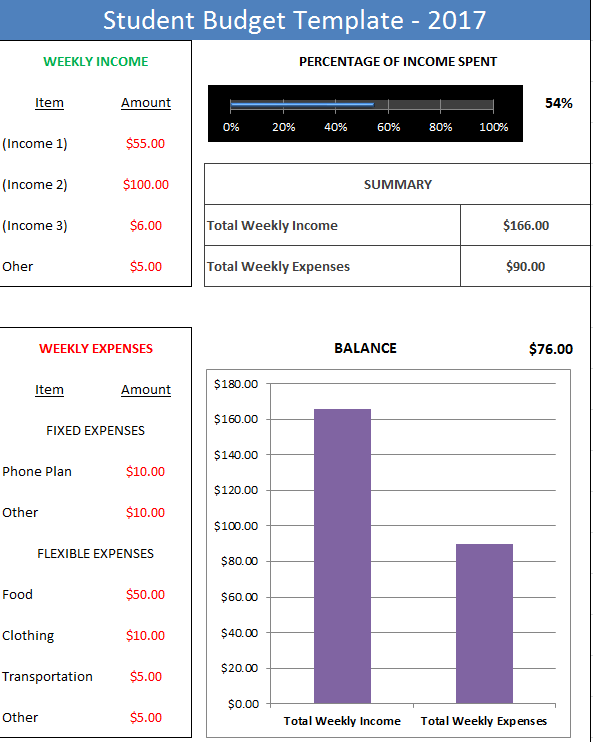

Here is an example of a simple weekly budget that I prepared.

Simply change the numbers in RED and the graphs will change automatically by themselves.

Fixed expenses vs flexible (variable) expenses (Phone plans vs holidays/food)

In the example budget above, expenses are divided into fixed and flexible sections.

One of the easiest ways to save money and keep your budget in check is to lower your fixed expenses. This includes your regular bills and regular payments that you must pay each month.

Unless you’re paying rent, your most significant fixed expense will be your phone plan. Try to shop around for a $40 phone plan. I decided that it was worth having an iPhone or Samsung phone that was one model behind the current model. For example, I discovered that if I bought the iPhone 6 when the iPhone 7 came out, I would get a much better deal.

Keeping your fixed expenses low allows you to budget more money for variable expenses i.e. food or entertainment, and also allows you to increase the amount of money you save each week. This leads us to the concept of savings goals.

When can you/should you get a bank account?

A baby can legally open a bank account (assuming they have a parent’s signature) from the day they are born.

(Alternatively, you can open your own bank account solo at age 18). Why should you have a bank account?

A bank account provides you with:

- Formal identification

- Access to your money

- An ability to earn interest on your money

- An online platform to set savings goals as well as a method for conducting and monitoring online transactions easily

Did you know? – According to the world bank, half the world’s adults, over 2.5 billion people, do not have a formal bank account.

In some sense, the ability to open a bank account is a privilege that not everyone has access to.

I would recommend setting up a savings account (if you haven’t already) as these accounts generally offer reasonable interest rates and do not charge a monthly account fee (but make sure you check this! – 31% of people aged 18 to 24 years do not take any steps to minimise their bank fees!).

When you set up a savings account with one of the big four Australian banks; Commonwealth Bank, ANZ, Westpac, NAB or others you will generally receive a debit card immediately. This will attach to one of your two online accounts and provides direct access to your money.

Only move a small portion of your money over to the account that is linked to your card as the interest will be significantly lower.

I recommend setting up a PIN (Personal Identification Number) that is 5 or 6 digits long (this was changed from the usual 4 digits) and make sure you avoid using your birthday as your PIN.

Credit vs Debit Card

Which card should I get?

These cards physically look similar except for a small difference, in the corner, one of them says credit, and the other says debit, so what’s the difference?

When you pay for something using a debit card (I’ll get to this in a second), you are using your own money from your own account.

On the other hand when you are using a credit card you are using money that is not yours. You are technically paying for the transaction using money from the bank with a promise (or a financial obligation) to pay the bank back with interest at a later date.

I would highly recommend starting off with a debit card only as you receive many of the benefits of electronic transactions without the high penalties associated with a credit card. Furthermore if you are careful with using the debit card online and only place a small portion of money on the account linked to the card your risk of having money stolen online will be low.

Interest rates

Would you rather be given $100 today, or $101 in 5 years time? If you are like most people you would rather be given the $100 today. Why? Because having money today is more valuable than having money in the future, or as the saying goes, a dollar today is worth more than a dollar tomorrow.

Fundamentally, an interest rate is the cost of borrowing money, and it is based on this principle. Most interests rates are written as a percentage per annum (% p.a.) which means it is the cost of borrowing an amount per year.

For example a 5% per annum interest rate on $100 would give you $5 interest in one year (assuming simple interest).

Generally the more access you will have to your money, the lower the interest rate. And vice versa. Currently a good savings account interest rate would be 3.5% per annum. The important thing about interest rates is that it helps you if you are saving money and works against you if you are borrowing money.

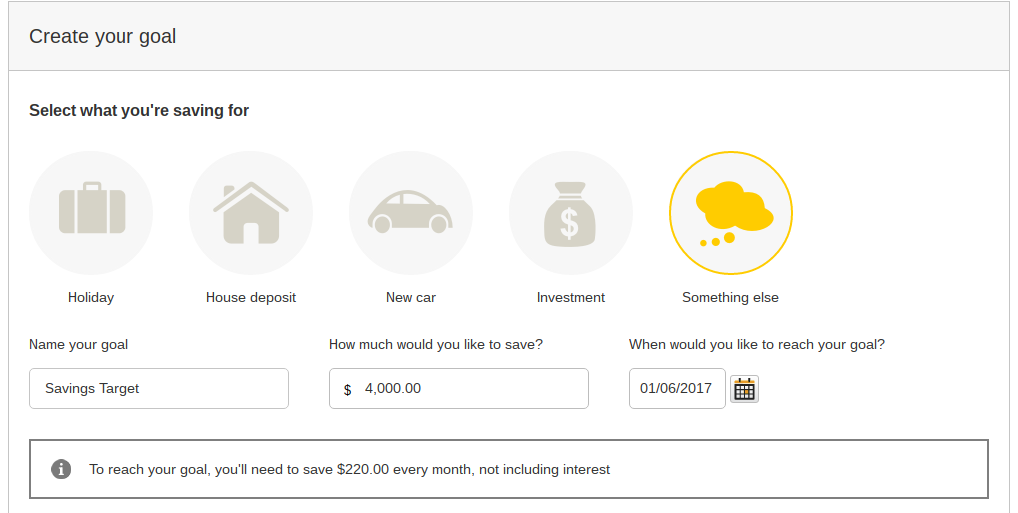

Savings Goal

Setting up a savings goal is relatively straight-forward and lets you track your progress on a regular basis.

I like to set up a savings goal within my actual savings account. Here is one I made on my savings account in less than two minutes!!

There are also great online calculators such as one available here.

Don’t Trust yourself? – Term Deposits

If you don’t trust yourself sometimes with your savings, a sneaky way to limit your spending is to put some of your money into a term deposit.

A term deposit ‘locks’ $1000 or more away at a time (generally for a period of 6 months to a year) and gives you a higher interest rate in exchange for you not being able to access/spend that cash.

This is a great way to make you spend less whilst rewarding you for doing so.

I think it’s a win-win.

Finally, here is a list of actionable items that you can do now to get ahead in life and feel in control of your money.

| Word | Definition |

|---|---|

| Budget | A budget helps you determine what your total income is, what your total expenditure is, and how much you have left over to save and spend on other things later. |

| Credit Card | A plastic card issued by a bank allowing the cardholder to purchase goods or services immediately on credit (with the bank's money - note: must be paid off/short-term loan) |

| Debit Card | A plastic card issued by a bank allowing the person to transfer money electronically from their bank account when making a purchase. |

| Financial Literacy | Ability to stay in control of finances and make short and long-term choices with money that positively impact one's life. |

| Interest | Money paid every month into a savings account. The amount depends on the rate of interest (% p.a.) and the amount of money in the account. Interest is a reward for saving and a cost of using a credit card. |

| PIN | Personal Identification Number - 4, 5, or 6 digit number used to protect and access your account. |

| Savings Account | A deposit account that pays reasonable interest. Normally issued with a linked debit card that can make transactions with merchants and withdrawals from ATMs. |

Immediate Action Plan:

- Apply for a Bank Account – Apply for a savings account and a debit card at a bank that is convenient to you.

- Tax File Number – If you haven’t applied for one already, do so soon. You can apply for one at any Australia Post Office. Additionally, most schools offer a way to fast track this process through the reception. You can find out more here.

- Superannuation – All part time jobs will require you to have a superannuation fund set up, so if you know you will be applying for a part time job soon, setting up a super account now will save you a lot of time later.

So those are just the basics and there’s a lot more to learn but we’re here to help you.

Looking for some extra help with your HSC studies?

We pride ourselves on our inspirational HSC coaches and mentors!

We offer tutoring and mentoring for Years K-12 in a variety of subjects, with personalised lessons conducted one-on-one in your home or at our state of the art campus in Hornsby! Check out how our expert K-12 tutors in the Liverpool area can support you!

To find out more and get started with an inspirational tutor and mentor get in touch today!

Give us a ring on 1300 267 888, email us at [email protected] or check us out on Facebook!

Thomas Woolley loves Economics and Business Studies. He completed his HSC in 2013 and has been working at Art of Smart since 2014. He enjoys helping out his students whilst studying B Commerce / B Education at UNSW to become an actual economics/business studies teacher in 2018. Since high school Thomas has also learned to scuba dive, salsa dance, and he can fly a quadcopter like a pro. However, he still cannot skateboard.